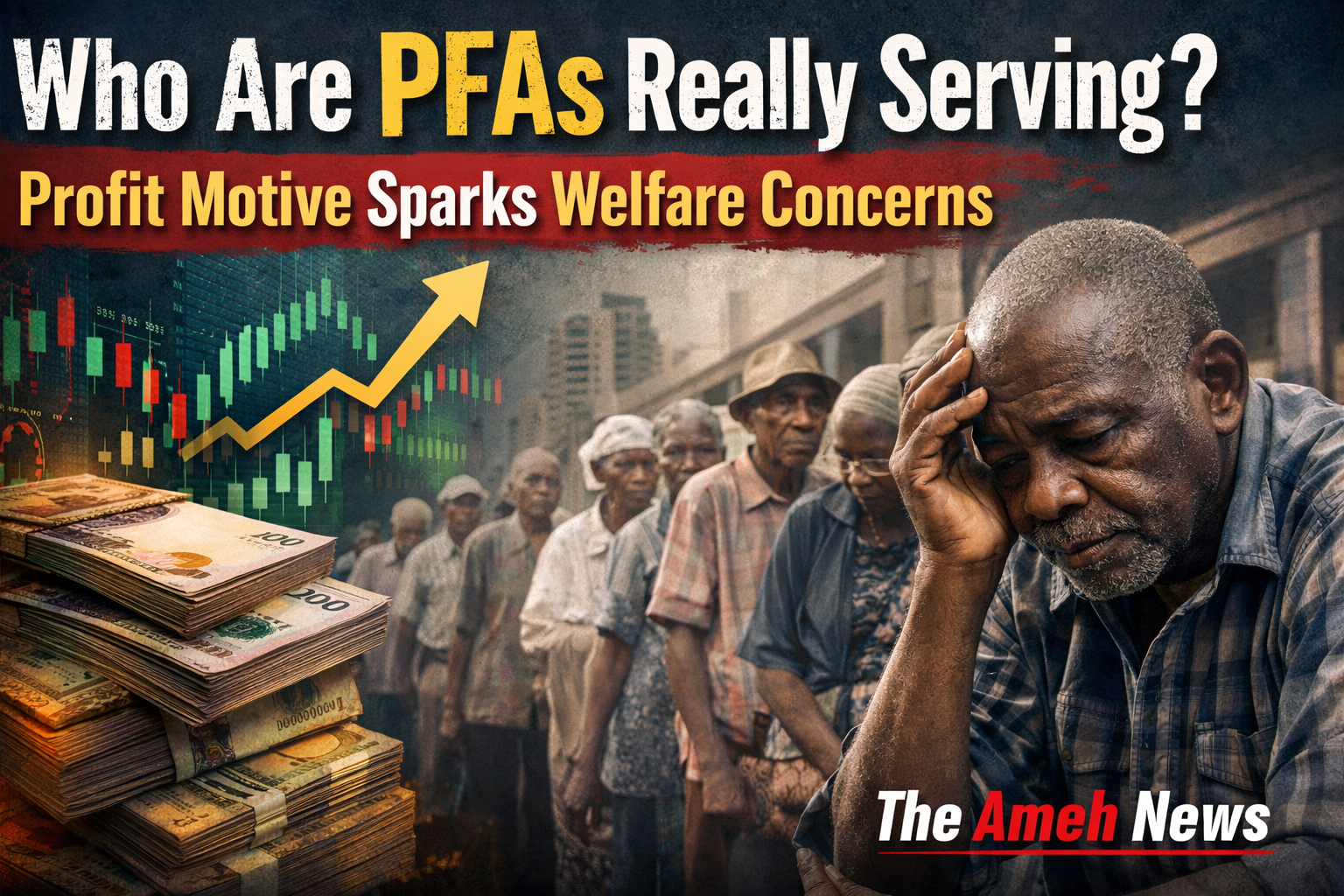

Nigeria’s pension system is financially growing, but many pensioners are not experiencing proportional improvements in their quality of life.This gap between asset performance and human welfare remains the central debate in the pension industry today.

Nigeria’s pension industry is witnessing unprecedented financial growth, with total assets now exceeding ₦28 trillion and equity investments alone rising to about ₦4 trillion. Pension Fund Administrators (PFAs) continue to deepen their presence in the capital market, positioning themselves as major institutional investors driving long-term economic financing.

Nigeria’s pension industry is witnessing unprecedented financial growth, with total assets now exceeding ₦28 trillion and equity investments alone rising to about ₦4 trillion. Pension Fund Administrators (PFAs) continue to deepen their presence in the capital market, positioning themselves as major institutional investors driving long-term economic financing.

Yet, amid this rapid expansion, a critical question is gaining urgency: Who is the pension industry really serving?

According to the report, this concern took centre stage during the First Quarter 2026 Pension Industry Leadership Council (PILC) press briefing today in Ikeja, Lagos, where the Director-General of the National Pension Commission (PenCom), Omolola Oloworaran, outlined the sector’s impressive performance metrics.

She disclosed that pension funds’ equity exposure now represents about 3 to 4 percent of the total market capitalisation on the Nigerian Exchange Limited (NGX), highlighting the industry’s growing influence in the equities market.

In her words, the ₦4 trillion equity allocation accounts for roughly 14 percent of the industry’s total pension assets, currently valued at over ₦28 trillion. The development reflects increasing confidence among PFAs in equities as a viable long-term investment class, she stresses.

Oloworaran also emphasised that increased pension investment in infrastructure would help bridge Nigeria’s infrastructure deficit, stimulate job creation, and enhance productivity across key sectors of the economy.

While these figures reinforce the narrative of a thriving and financially sophisticated pension system, they also expose a stark contradiction.

Across Nigeria, many retirees continue to grapple with delayed payments, inadequate pensions, and rising living costs that have significantly eroded their purchasing power. For them, the industry’s growth story feels distant—if not entirely disconnected—from their lived reality.

The contrast is striking: as PFAs grow assets and diversify portfolios, pensioners face mounting hardship.

The report further disclosed that Numerous retirees recount struggles to afford basic healthcare, housing, and daily sustenance. For individuals who spent decades contributing to the system, retirement has become less about comfort and more about survival.

Experts argue that this widening gap underscores a fundamental imbalance between financial performance and social responsibility.

According to Celestine Ukpong, the pension system risks losing its core purpose if growth is not matched with improved welfare outcomes. “The industry is clearly expanding, but the benefits are not translating to pensioners. A pension system must prioritize its beneficiaries, not just its balance sheet,” he said.

Similarly, Dr Ejike Nduilo warned that the current trajectory raises ethical concerns. “We are seeing strong returns and rising asset bases, yet retirees are struggling. That disconnect suggests the system is becoming more commercial than compassionate,” he noted.  “The core purpose of the pension industry is to provide income security and financial dignity in retirement. Not job creation, infrastructure funding, and capital market growth—is a by-product, not the main goal. What the Pension Industry is meant to do. At its foundation, a pension system exists to: Ensure workers receive steady income after retirement, Protect retirees from poverty and financial uncertainty, and Provide long-term financial stability after active employment

“The core purpose of the pension industry is to provide income security and financial dignity in retirement. Not job creation, infrastructure funding, and capital market growth—is a by-product, not the main goal. What the Pension Industry is meant to do. At its foundation, a pension system exists to: Ensure workers receive steady income after retirement, Protect retirees from poverty and financial uncertainty, and Provide long-term financial stability after active employment

Also speaking, Peter Adebayo called for a redefinition of success within the industry. “Performance should not be measured solely by trillions in assets. The real measure is whether pensioners can live with dignity. If they cannot, then the system needs urgent reform,” he stated.

At the centre of the debate is the increasing commercialization of pension management.

Over time, PFAs have adopted sophisticated investment strategies, channeling funds into equities, infrastructure, and other high-yield instruments. While this approach strengthens long-term sustainability and supports economic growth, critics argue it has also shifted focus away from the immediate needs of retirees.

The result is a system that appears financially robust but socially strained.

For pensioners, this imbalance has real consequences. The promise of a secure retirement is being overshadowed by uncertainty, frustration, and, in many cases, hardship.

Analysts say bridging this gap requires deliberate policy action.

Recommendations include ensuring prompt payment of benefits, adjusting pensions to reflect inflation realities, improving transparency in fund management, and creating mechanisms that directly link investment performance to pensioner welfare.

Without such reforms, the industry risks undermining public trust, regardless of how impressive its financial indicators remain.

Ultimately, the sustainability of Nigeria’s pension system will depend on its ability to balance profit with purpose.

As PFAs continue to grow assets and expand investment frontiers, the central question persists: who is truly benefiting from the ₦28 trillion pension boom?

Until retirees begin to experience tangible improvements in their quality of life, the business of retirement will remain, for many, a system that serves the market more than the people it was designed to protect.

Nigeria’s pension assets surpass ₦28 trillion with ₦4 trillion in equities, but retirees face hardship, raising concerns over whether PFAs are prioritising profits over pensioners’ welfare.

Discover more from Ameh News

Subscribe to get the latest posts sent to your email.