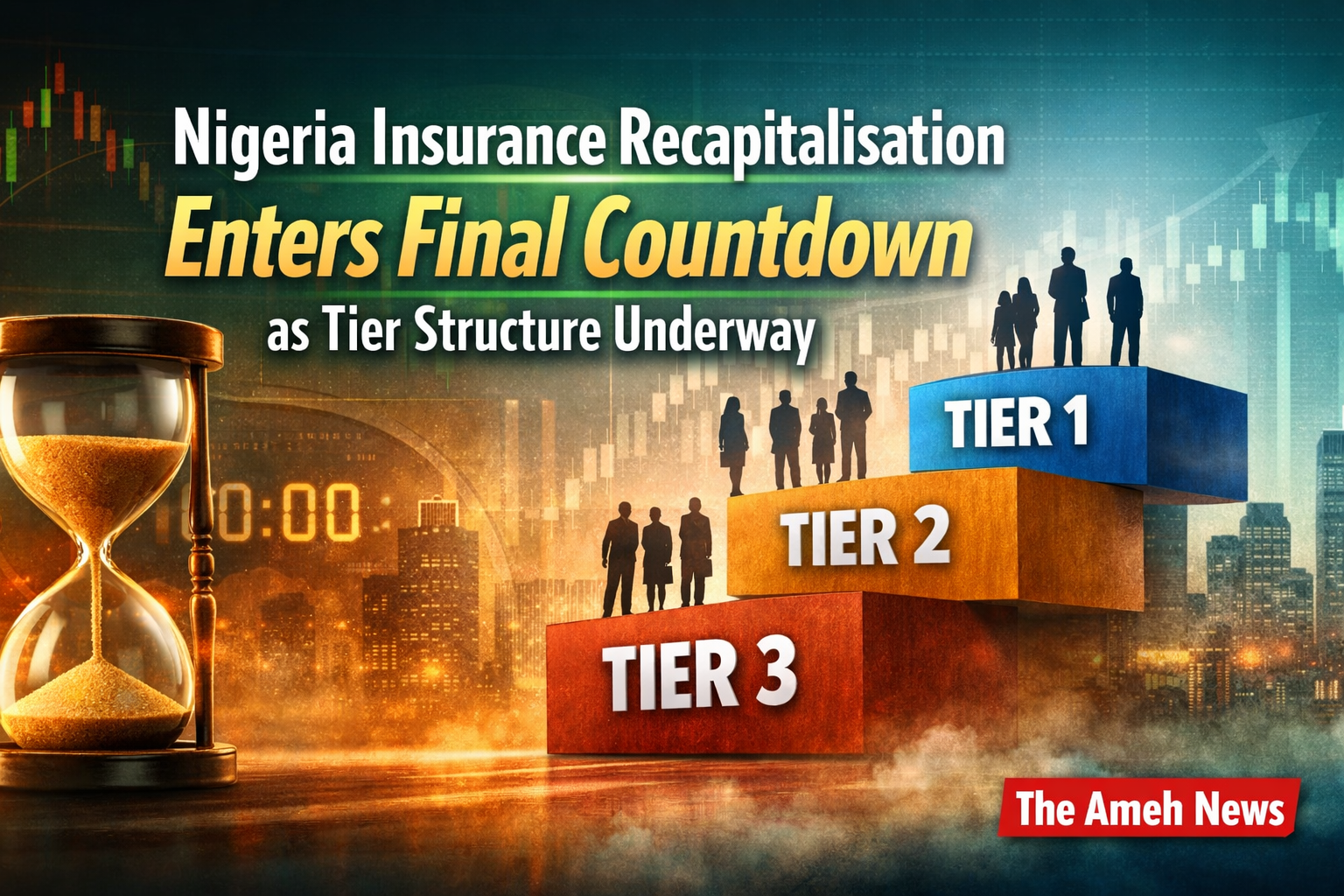

Nigeria’s insurance industry has entered the final stretch of its sweeping recapitalisation programme under the Nigeria Insurance Industry Reform Act (NIIRA 2025), with just 57 days remaining until the 31 July 2026 compliance deadline. The exercise, led by the National Insurance Commission (NAICOM), is now reshaping the sector into a clearly emerging three-tier structure, as firms race to meet significantly higher capital requirements.

Nigeria’s insurance industry has entered the final stretch of its sweeping recapitalisation programme under the Nigeria Insurance Industry Reform Act (NIIRA 2025), with just 57 days remaining until the 31 July 2026 compliance deadline. The exercise, led by the National Insurance Commission (NAICOM), is now reshaping the sector into a clearly emerging three-tier structure, as firms race to meet significantly higher capital requirements.

NAICOM has maintained a firm position that the deadline is final, binding, and non-negotiable, with no extension expected and no concessions for non-compliant operators. This stance has intensified pressure across the sector, pushing insurers into accelerated capital raising, investor negotiations, and merger discussions.

Industry analysts say the process has moved beyond regulatory compliance into a structural reset of the entire insurance ecosystem, where survival is increasingly determined by capital strength, execution speed, and access to funding.

New Capital Framework Driving Industry Restructuring

Under the revised regulatory regime, insurers are required to meet new minimum capital thresholds based on their operational category:

Life insurance operators for ₦10 billion

Non-life insurance operators for ₦15 billion

Composite insurance operators for ₦25 billion

Reinsurance operators for ₦35 billion

The framework also introduces a risk-based capital model, which links capital adequacy directly to underwriting exposure and risk profile rather than flat minimum requirements.

Analysts say this shift is aligning Nigeria’s insurance market with global solvency standards and is expected to significantly strengthen underwriting capacity in the medium to long term.

Market Reality: Uneven Compliance and Rising Pressure

As the deadline approaches, compliance across the industry remains uneven. While some operators have advanced capital-raising strategies through investors, rights issues, or internal restructuring, others are still in early or mid-stage execution.

The result is a market under increasing strain, where timing, investor access, and capital market readiness are becoming decisive survival factors.

Market observers say the sector is now firmly in an execution phase, not a planning phase.

Emerging Tier Structure: Nigeria Insurance Market Reorganises in Real Time

Analysts are increasingly describing the industry as reorganising into a three-tier system, reflecting varying levels of capital strength and compliance readiness.

Tier 1: Strong Capital Base and Potential Consolidators:

This group includes insurers with strong balance sheets, better access to capital markets or strategic investors, and relatively lower recapitalisation pressure.

Characteristics of this tier include:

Strong solvency positions

Ability to absorb or acquire weaker players

Reduced dependence on urgent capital raises

Strategic flexibility in mergers and partnerships

These firms are expected to play a central role in shaping post-recapitalisation industry structure as potential consolidators.

Tier 2: Active Recapitalisation and Capital-Raising Group:

This segment includes insurers actively pursuing compliance through:

Rights issues

Private placements

Shareholder injections

Ongoing investor negotiations

These operators are not necessarily distressed but are under time-bound pressure to complete capital formation before the deadline.

Key characteristics:

Mid-tier capital strength

Active engagement with capital markets

High sensitivity to timing and investor appetite

Elevated exposure to merger discussions if delays occur

Tier 3: High Pressure and Consolidation Candidates:

This group represents insurers facing the greatest pressure to meet capital requirements independently.

Characteristics include:

Weak or insufficient capital buffers

Heavy reliance on last-minute fundraising

Limited access to strong strategic investors

Higher probability of merger, acquisition, or restructuring outcomes

Analysts say this tier is most exposed to post-deadline regulatory enforcement actions if compliance is not achieved.

Expert Insight: Structural Reset Already Underway

Speaking with The Ameh News, economist Celestine Ukpong said the recapitalisation programme represents one of the most significant reforms in Nigeria’s insurance industry in decades, arguing that the emerging Tier 1, Tier 2, and Tier 3 structure reflects the realities of capital strength, investor confidence, and compliance readiness.

“The tier-based outcome should not be viewed as a weakness of the industry. Rather, it is evidence that capital discipline is beginning to shape the market. Ultimately, the sector may have fewer operators, but those that remain will be stronger, better capitalised, and more capable of underwriting major economic risks,” he said.

Ukpong explains further that the reform will likely produce:

“A smaller number of insurers, but with significantly stronger capital bases, improved underwriting capacity, and greater systemic resilience.”

Ukpong adds that the reform could improve the sector’s ability to support long-term financing of infrastructure, energy, and sovereign-linked risks if fully implemented.

Financial Analyst View: Timing Is Now the Decisive Factor

Also, speaking with The Ameh News, Peter Adebayo, FCA, noted that the industry has entered what he described as the ‘execution phase’ of recapitalisation, where timing, regulatory approvals, investor commitments, and market confidence are proving just as important as access to capital itself.

“As the deadline draws closer, insurers are operating under increasing pressure. Those with well-structured capital plans and strong investor support are likely to navigate the process successfully, while operators that delay critical decisions may find themselves with fewer strategic options. This is why the market is beginning to witness heightened merger and acquisition conversations.”

He added that the recapitalisation exercise is likely to leave behind a more resilient and better-capitalised insurance industry, capable of underwriting larger risks and supporting Nigeria’s long-term economic growth objectives.

Adebayo notes:

“The key dividing line is no longer who has access to capital, but who can complete the process before the deadline. Timing risk is now the biggest threat to independent survival.”

Adebayo adds that the market is likely to experience a surge in mergers and acquisitions, particularly as weaker operators seek strategic partners to avoid regulatory penalties.

Market Outlook: Consolidation Becoming Inevitable

With NAICOM maintaining its strict position—no extension and full enforcement after the deadline—the insurance sector is entering a decisive restructuring phase.

Expected outcomes include:

Accelerated capital raising activity in the final weeks

Increased merger and acquisition negotiations

Regulatory verification and enforcement after deadline

A more concentrated but financially stronger insurance industry

Nigeria’s insurance recapitalisation exercise has evolved from a regulatory compliance initiative into a full-scale market restructuring event. The emergence of a clear Tier 1–3 structure reflects the growing divide between capital-strong operators, active raisers, and high-pressure firms.

Nigeria’s insurance recapitalisation exercise has evolved from a regulatory compliance initiative into a full-scale market restructuring event. The emergence of a clear Tier 1–3 structure reflects the growing divide between capital-strong operators, active raisers, and high-pressure firms.

As the countdown continues, the industry’s defining outcome will not simply be compliance—but the reshaping of Nigeria’s insurance landscape into a more concentrated, capital-strong ecosystem.

Nigeria’s insurance sector enters a 57-day recapitalisation countdown under NIIRA 2025 as NAICOM maintains no-extension policy, driving a Tier 1–3 market structure, rising consolidation pressure, and full industry restructuring.

Both Celestine Ukpong and Peter Adebayo, agree that Nigeria’s insurance recapitalisation exercise has evolved beyond a regulatory compliance requirement into a defining restructuring moment for the industry.

While Ukpong views the emerging tier-based market structure as a natural outcome of stronger capital discipline and regulatory reforms, Adebayo believes the ultimate determinant of success will be how effectively insurers execute their recapitalisation plans before the deadline.

Together, their assessment points to a common conclusion:

The future of Nigeria’s insurance industry will be shaped not merely by access to capital, but by the ability of operators to meet regulatory requirements on time, adapt to a more demanding risk-based framework, and position themselves for a more competitive and consolidated market. The likely outcome is a smaller but stronger industry, with better-capitalised insurers capable of underwriting larger risks, strengthening policyholder confidence, and contributing more meaningfully to Nigeria’s economic development.

As the countdown to the July 31, 2026 deadline continues, the sector stands at a critical crossroads where capital strength, strategic execution, and regulatory compliance will determine the winners of Nigeria’s next insurance era.

Key takeaway:

Nothing is “missing” for those companies that they are simply in different survival lanes:

Strong firms → stabilising and positioning as buyers

Mid-tier firms → racing to raise capital

Weak firms → facing merger or takeover pressure

Discover more from Ameh News

Subscribe to get the latest posts sent to your email.